In California, milk production has been trending weaker recently. Handlers indicate September 2024 milk output is above September 2023 milk output, but below anticipated volumes and down compared to last month. Stakeholders convey spot milk loads can be found for buyers looking to fill needs, but spot milk loads are not abundant. Class III demands are strong. All other Class demands are steady. According to the California Department of Water Resources, as of September 17, 2024, the state precipitation total for the 2023-24 Water Year, which ends on September 30, 2024, is 23.74 inches. The current precipitation total is .27 inches above the historical mean. According to the California Department of Water Resources, as of September 18, 2024, the estimated total statewide reservoir storage is 25.00 million- acre feet, which is 114 percent of the historical average for the month.

Farm level milk output is steady in Arizona. Stakeholders describe milk volumes as tight. All Class manufacturing demands are steady.

Milk production in New Mexico is noted as stronger. However, milk volumes remain tight in this part of the southwest as well. Demands for all Classes are steady.

Handlers in the Pacific Northwest indicate steady or stronger milk production. Manufacturers convey milk volumes are meeting processing needs. Spot milk availability is tighter this week. Class I demand is stronger. Class II, III, and IV demands are steady.

Farm level milk output in the mountain states of Idaho, Utah, and Colorado varies from steady to stronger. Stakeholders suggest looser availability of spot milk loads this week. Manufacturers suggest milk volumes are healthy compared to production needs. All Class demands are unchanged.

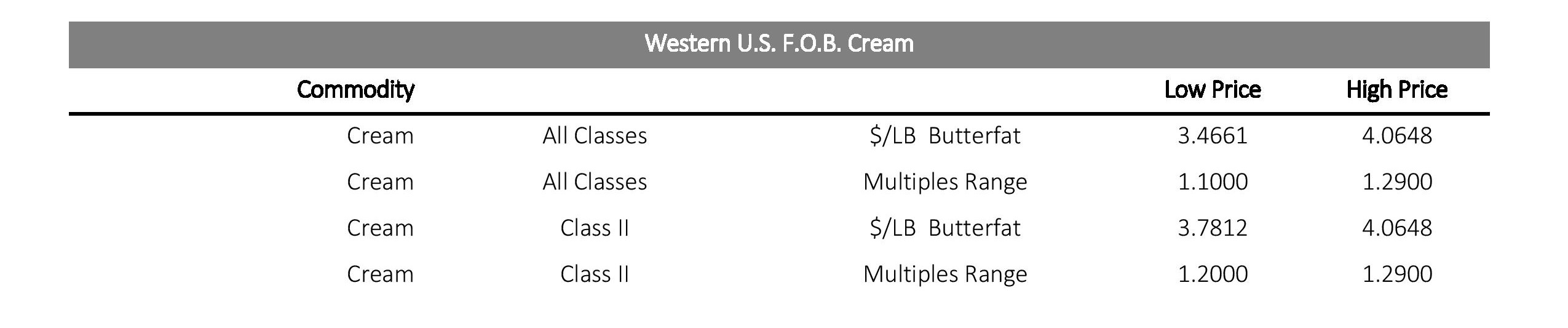

Cream volumes are generally available in the region, more so than other parts of the country. Cream demand varies from steady to lighter. Cream multiples moved slightly lower on the top end of both ranges. Condensed skim milk demand and availability has not changed from last week.