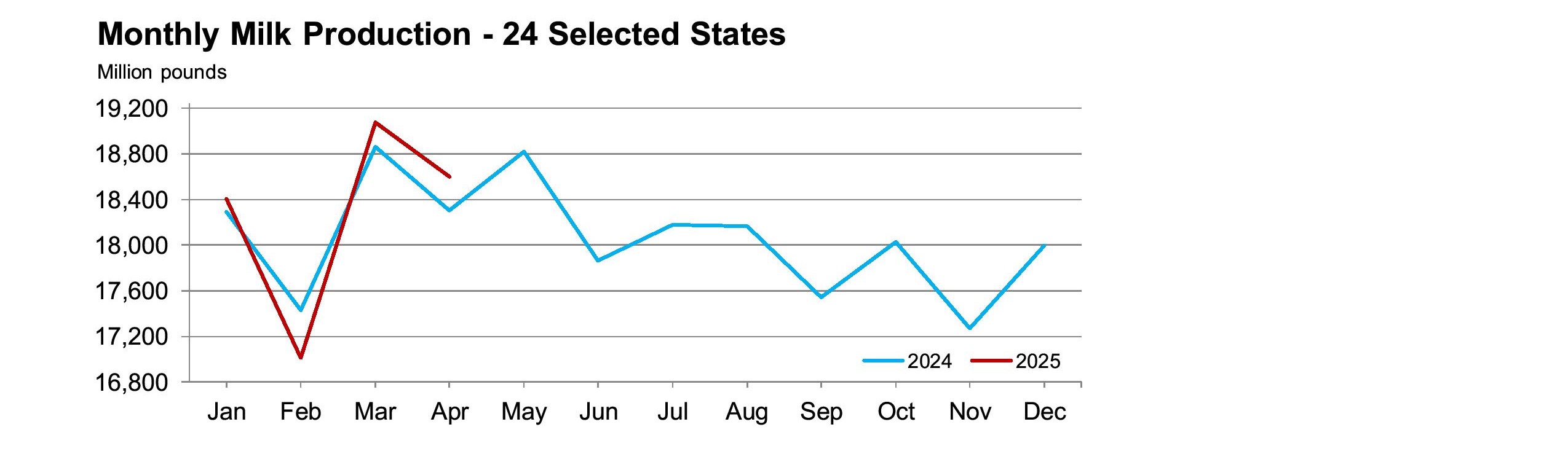

MILK:

It has been a volatile, holiday-shortened week with Class III milk futures closing lower than a week ago. Class IV futures closed higher. Market fundamentals have not changed, but buyers in the spot market turned aggressive, pushing prices higher. Class III futures are higher than Class IV through July and are near the same price for August. The butter price has been strong over the past week but has not been able to distance itself from the cheese prices. The April Agricultural Prices report was released today. The average corn price was $4.62 per bushel, up $0.05 from March and $0.23 higher than April 2024. The premium/supreme hay price was $252.00 per ton, up $10.00 per ton from March but $8.00 per ton below a year ago. The All-milk price was $21.00 per cwt, down $1.00 from March, but up $0.60 from April 2024. The average soybean meal price will be released on Monday by the FSA. That is when we can calculate the income over feed price for the Dairy Margin Coverage program.

AVERAGE CLASS III PRICES:

| 3 Month: | $19.14 |

| 6 Month: | $19.27 |

| 9 Month: | $19.11 |

| 12 Month: | $18.91 |

CHEESE:

For the week, blocks gained 7.75 cents with 26 loads traded. The weekly average price was $1.9413. Barrels gained 1.75 cents with 13 loads traded. The weekly average price was $1.8675. Dry whey gained 3 cents with nine loads traded. The weekly average price was 56.81 cents. The trading activity in cheese took place over three days, with no trading activity and no interest shown in spot trading today.

BUTTER:

For the week, butter gained 5.50 cents with 39 loads traded. The weekly average price was $2.4938. Grade A nonfat dry milk gained 3.50 cents with 14 loads traded. The weekly average price was $1.2819. Churning remains active with a sufficient cream supply despite ice cream production increasing ahead of the summer and using a significant amount of cream.

OUTSIDE MARKETS SUMMARY:

July corn closed down 3.00 cents per bushel at $4.4400, July soybeans closed down 10.00 cents at $10.4175 and July soybean meal closed down $.10 per ton at $296.30. July Chicago wheat closed steady at $5.3400 and August live cattle closed down $0.73 at $209.35. July crude oil is down $0.15 per barrel at $60.79. The Dow Jones Industrial Average is up 54 points at 42,270, with the NASDAQ down 62 points at 19,114.